It feels like I’ve seen this at least once a month for the past year, but gold and silver hit near-record highs this week… again. The US also conducted military operations in Venezuela, which raises some questions about the global oil supply. ISM data showed manufacturing continues to struggle while services thrive, but that’s not exactly a surprise. Warner Bros rejected Paramount’s massive LBO in favor of Netflix’s deal. It’s honestly the right call given the equity involved, which lowers their overall risk. And finally, I’ll explain one of the most used terms in finance and why it’s important in this week’s educational topic.

This week, I’ll address the following topics:

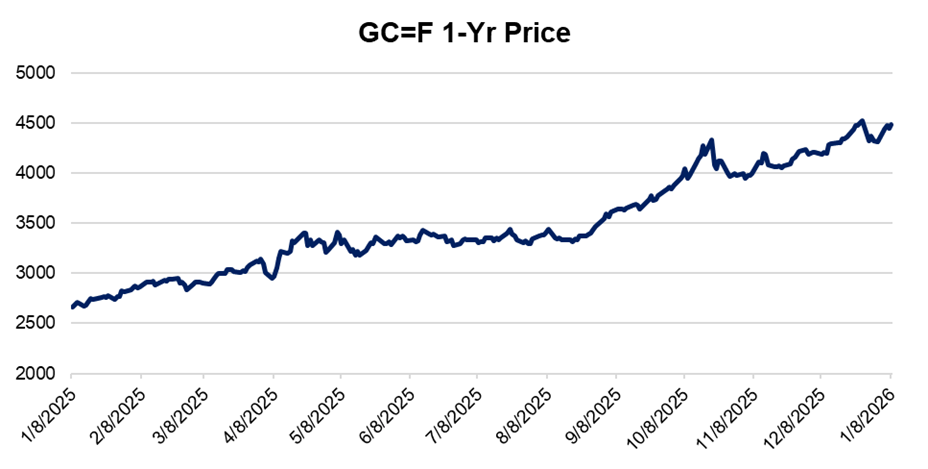

- Gold climbs above $4,400 and silver reaches the mid-$70s. Geopolitical tensions and industrial demand are driving precious metals higher.

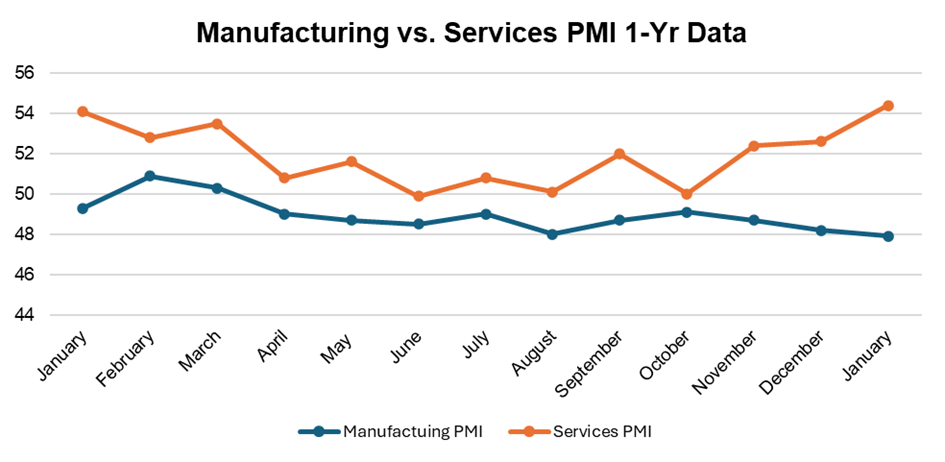

- ISM Manufacturing stays in contraction at 47.9 while Services beat expectations at 54.4. The divergence between these sectors continues.

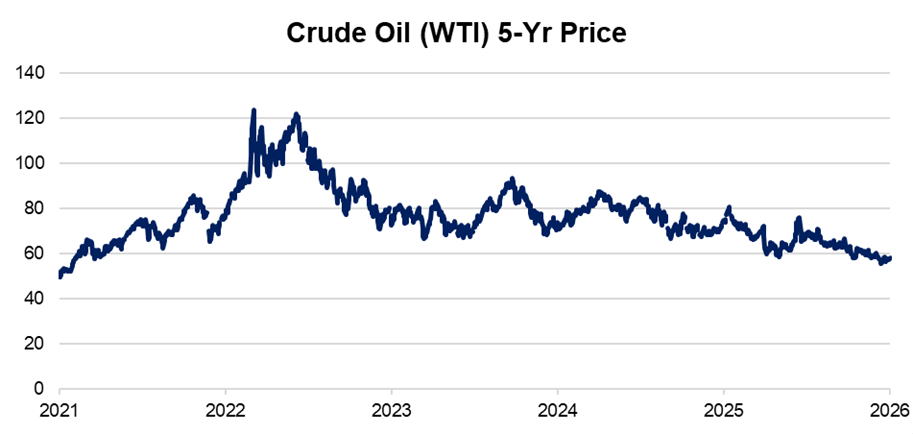

- US military operations in Venezuela create uncertainty around oil exports. What does this mean for supply and prices?

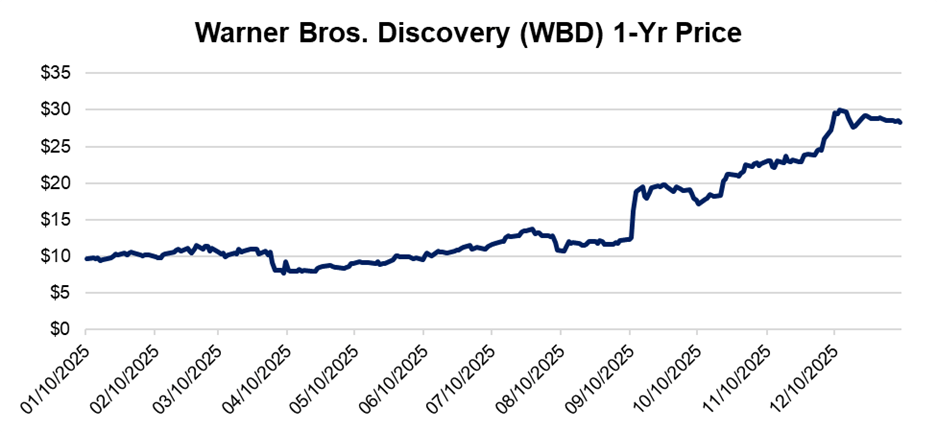

- Warner Bros rejects Paramount’s $108 billion bid for the second time, sticking with Netflix. The debt levels in Paramount’s offer would have been catastrophic.

- In our educational topic, we explain EBITDA and why it’s crucial for comparing companies and understanding valuation.

1) Gold & Silver Surge

Gold and silver have surged this week amid rising geopolitical tensions, particularly surrounding US–Venezuela relations. Gold has climbed near record levels above $4,400 per ounce while silver has climbed toward the mid-$70s. Investors are moving towards precious metals not only as protection against potential instability but also in anticipation of looser monetary policy and weaker macroeconomic data.

Source: Yahoo Finance

My Takeaway: The demand for silver has skyrocketed over the past year following the demand for data centers, EV, and other growing industries that require it in bulk. As we head into 2026, this trend is only set to continue as we see the realization of billions of dollars in Capex from some of the largest companies in the world as they continually invest into AI. This has also caused a structural shortage as demand for outpaced supply, causing stockpiles and inventory to decrease. For those reasons, I would expect silver to become more expensive in the new year. As far as gold’s performance, this comes in the wake of international tensions between the US and Venezuela. But more than that, it’s been a signal of investor uncertainty for a while now. Outside of the past two months, most inflation and labor metrics were exclusively negative throughout most of 2025, which continually drove up its value (though no one could’ve reasonably predicted it would jump like this). Whether that continues in 2026 is yet to be decided, and while gold is always one of the safest assets to invest in, it’s highly unlikely we’ll see a similar skyrocket in value like we did last year.

2) ISM Services and Manufacturing PMI

Recent U.S. economic data paints a mixed picture of the domestic economy. The ISM Manufacturing PMI stayed in contraction territory at 47.9, while on the other hand, the Services PMI came in at 54.4, which was significantly higher than the forecasted 52.2.

Source: Forex Factory

My Takeaway: TheManufacturing PMI hasn’t been on the plus side of 50 since last March, while the Services hasn’t been on the downside since last June. These two sectors are clearly headed in opposite directions, but there’ nothing new about this. This is in part due to the effective tariff rate raising input costs as well as counter-tariffs being placed (ironic since they were supposedly meant to help manufacturing), but we’ve known for a while now that manufacturing and blue-collar jobs have been suffering in the US. Much of the work is being outsourced. This is a trend that I’ve been hearing my entire life, and it feels as though we go through every election cycle with the same discussion. It would be nice to see some change, but I doubt it’ll come soon. The service sector’s growth also comes as no surprise as they’ve been leading the game for a while now. Last year we saw the AI boom, along with record bank earnings, and billion-dollar deal after billion-dollar deal.

3) Venezuela, the US, and Oil

Tensions with Venezuela jumped this week, with potentially substantial effects on oil markets. The U.S. conducted military operations in Venezuela on January 3rd and detained President Nicolás Maduro on drug trafficking and weapons charges. This has created uncertainty around Venezuelan oil production and exports. Venezuela has the world’s largest oil reserves, but its capitalization on it has been poor, in part due to Maduro’s policies and operations, which have also caused sanctions and lack of investment. The big questions now are what happens to Venezuelan oil exports and who gets access to them.

Source: FRED

My Takeaway: The US is putting immense pressure on the nation to partner directly and give preference to them for all oil exports. President Trump has also said that Venezuela will be giving the US close to $3 billion worth of oil. With the US in direct control of the country indefinitely (or so they say), companies here are in position to take advantage of additions to their stockpiles. However, I don’t think this would lower prices. For one thing, I doubt the government would immediately flood the market with oil, and for another, oil prices going below President Trump’s target of $50 is unrealistic as it would put companies in a profitless position. Regardless, whether we get most of the oil is still completely up in the air. The geopolitical tensions alone (which are completely different conversations) are cause for uncertainty but combining that with the spontaneity of the current administration makes it very difficult to predict what could happen from here on out. In any case, it’s imperative to keep an eye on this situation.

4) Warner Bros. Stays Set on Netflix

Warner Bros. board unanimously rejected a revised $108.4 billion acquisition bid from Paramount. They had concerns over the deal’s excessive leverage and the financial risk it would impose on shareholders. At the same time, Warner Bros. encouraged its shareholders to stay on the course with the deal it already has with Netflix. This is the second time Warner Bros. has rejected an acquisition bid higher than Netflix’s.

Source: Yahoo Finance

My Takeaway: It would cost Warner Bros. billions to stop their deal with Netflix, and more than that, the Paramount Deal would be the largest LBO in history if it went through. The estimated debt involved would be over $85 billion, significantly higher than the recently set record in the EA acquisition a couple of months ago of $55 billion. For those reasons alone, I think the Netflix deal is by far more attractive. Their financing includes a much greater share of equity, which is inherently less risky for Warner Bros. From Netflix’s perspective, the deal is estimated to bring in close to $5 billion in recurring revenue from HBO subscribers, not to mention the additions of other IP such as Looney Tunes, DC Universe, and Harry Potter/Wizarding World libraries, so I’d say it’s a win for them.

5) Educational Topic: EBITDA and Why It’s So Important

EBITDA stands for Earnings before Interest, Taxes, Depreciation, and Amortization, and it’s one of the most important metrics in finance. First and foremost, it measures the core profitability of a company, as it doesn’t account for any of the very variable factors companies face. For that same reason, it’s also a good measure of comparing companies across separate industries. For example, an industrials company would likely face much higher depreciation costs than a SaaS company would be due to their asset heavy nature. Companies in different geographic areas would also face different tax rates. Since all these factors change significantly due to the company’s industry, using EBITDA allows us to make the fairest comparison. EBITDA is also important from a valuation’s perspective. EV/EBITDA is often considered the best multiple to use since it focuses on core profitability (as mentioned before) and it’s also capital structure neutral. Changes in capital structure do not affect Enterprise Value (since a change in debt would cancel with the according change in cash) nor EBITDA (a change in debt would affect interest payments, but those are not included in EBITDA).

Leave a comment