Before I start, quick shoutout to Miranda for suggesting this topic. Would love to hear more ideas in the suggestions box. Thanks for the idea!

What are Roth IRA Accounts?

First off, there’s a difference between IRA and Roth IRA accounts. In principle, they are both types of investment accounts, but Roth IRAs are normally meant for those who expect to be in higher tax brackets by the time they retire. This will be explained more in the next section.

An IRA stands for Individual Retirement Account, and it’s exactly what it sounds like: a savings account for retirement. A Roth IRA is a tax-advantaged savings account designed to help people save for retirement. Unlike most retirement accounts, contributions to a Roth IRA are made with after-tax dollars. After that, your investments grow completely tax-free, and withdrawals in retirement are also tax-free. Since there’s no tax, there are limits put on how much you can contribute up. The maximum amount is $7,000/year, or $8,000 if you’re 50+. Roth IRAs also come with flexibility. Since you’ve already paid taxes on your contributions, you can withdraw the amount you contributed at any time, penalty-free.

What’s the Difference Between a Roth IRA and a Traditional IRA?

The main difference between a Roth and a traditional IRA is when you get your tax break. With a Traditional IRA, contributions may be tax-deductible in the year you make them, which lowers your taxable income now. But you’ll owe income taxes on your withdrawals in retirement. The Roth IRA flips this, since your investments are made with after-tax income, and withdrawals in retirement are tax-free. This makes the choice largely a bet on your future tax situation. If you expect to be in a higher tax bracket when you retire than you are today, choose a Roth IRA, since you lock in today’s lower rate rather than paying a higher one later. But if you’re currently in a high tax bracket and expect to be in a lower one in retirement, a Traditional IRA’s upfront deduction is likely the better option, since you can pay lower tax later.

One last important note: There are income limits to Roth IRA accounts. Starting around $160k for single and $240k for married-joint filers, Roth IRAs begin what’s called a “phase-out”, which is a gradual reduction in your maximum investment until it hits $0 at a point. However, with a traditional IRA, anyone can contribute regardless of income, but higher earners may lose the ability to deduct those contributions from their taxes.

Are There Any Advantages to Opening Them Early?

This section comes directly from Miranda’s question, which asked about opening a Roth IRA at 18.

A Roth IRA can be opened by anyone at any time, as long as you have an income. Like with any savings account, the earlier you start saving, the greater the long-term effect. You’ll start earning compounded growth that keeps going for decades. The benefits of specifically having a Roth IRA this early are that they offer much higher growth than a typical savings account, since they are more accurately described as an investment account. IRAs invest your money into stocks, ETFs, and more. Beyond that, they’ll give you flexibility long-term since there aren’t penalties for certain withdrawals. The fact that this growth isn’t taxable either is also a huge benefit. Beyond that, you’re probably not at the peak of your earnings or tax bracket as an 18-year-old, which further bolsters the appeal of a Roth IRA for you.

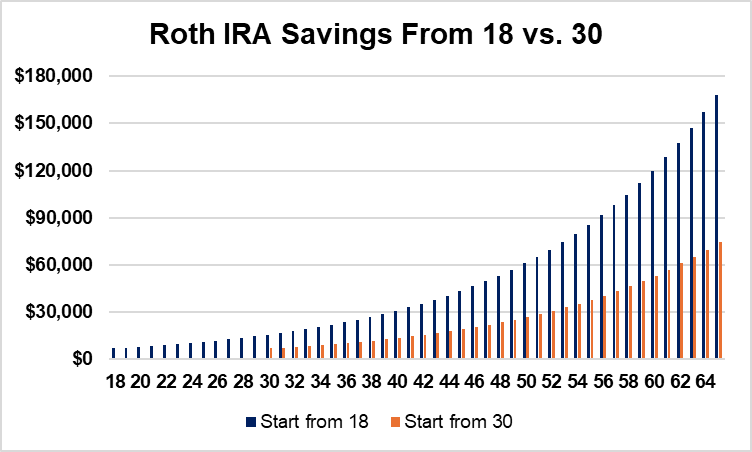

Below is an example of investing $ 7,000 at 18 vs. 30, and how it would turn out by retirement at 65, assuming a 7% return and no additional investment.

It’s a huge difference, so it’s probably a good idea to start as early as possible!

Disclaimer:

This blog post is for educational and informational purposes only. It is not financial advice. I am not a licensed financial advisor, and nothing in this post should be interpreted as a recommendation to buy or sell any securities. Trading involves risk, and results are not guaranteed. Past performance is not indicative of future results. Always do your own research and consult with a licensed financial professional before making any investment decisions.

Leave a comment